Case Study • Lending • AI-Assisted Underwriting Automation

70% time saved in verification + underwriting

Omovera automated end-to-end verification across KYC, bank statements, income proof, bureau data, and policy checks—so expert underwriters focused on exceptions, risk judgment, and governance.

Client details anonymized. Outcomes and methods are representative.

Business outcomes

The win wasn’t “automation” by itself. It was shifting expert effort to higher-order judgment—while improving control.

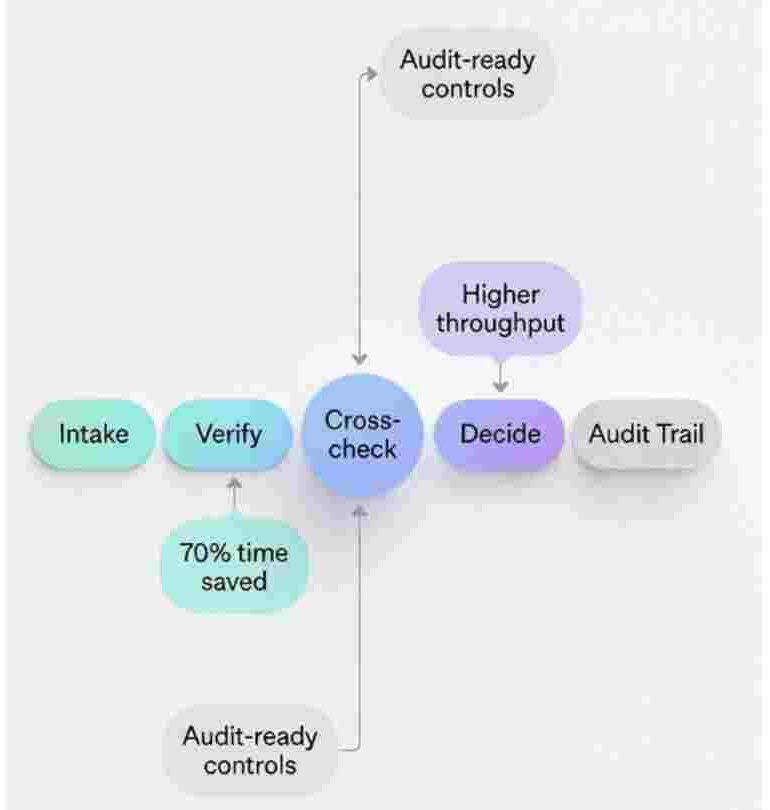

~70% reduction in verification and underwriting effort via extraction, validation, and policy checks.

Experienced analysts focused on exceptions, complex profiles, and policy decisions—rather than manual reconciliation.

More consistent checks, traceable reasoning, override paths, and standardized decision evidence.

Before vs after (what changed)

A simple way to explain transformation to your board and leadership team.

- • Manual extraction from PDFs and images

- • Repetitive checks done inconsistently

- • Underwriters spending time on “data gathering”

- • Limited traceability for exceptions and overrides

- • Automated extraction and structured evidence

- • Standardized checks + cross-validation

- • Experts focused on exceptions and risk judgment

- • Strong audit trail and clear decision rationale

What we built (simple to understand)

A pipeline that turns messy documents into decision-ready signals—while keeping humans in control.

- • KYC extraction + verification checks

- • Bank statement parsing: salary, bounces, obligations, trends

- • Income proof extraction: salary slip consistency & anomalies

- • Bureau ingestion: score, delinquencies, vintage, mix

- • Salary slip ↔ bank credits matching

- • EMI detection ↔ bureau tradelines

- • Employment signals ↔ cash-flow patterns

- • Flags for contradictions, gaps, suspicious patterns

- • Policy checks and eligibility gates

- • Risk summary for the underwriter

- • Recommendation with reasons + evidence

- • Exception routing to human review

- • Workflow: intake → verify → decide → approve

- • Structured notes + audit trail generation

- • Override and escalation path design

- • Monitoring and continuous improvement loop

Technical deep dive (optional)

Enough technical detail to satisfy CIO/CTO and risk stakeholders—without turning this into an engineering document.

A staged pipeline: ingest → extract → normalize → validate → score → recommend → route. Each stage has quality thresholds and fallbacks.

The system returns structured fields + supporting evidence (source doc, page/line, confidence), so decisions remain defensible.

Low confidence, missing docs, contradictions, or policy edge cases automatically route to underwriter review with a clear “why” and recommended next actions.

How we typically implement (example roadmap)

A pragmatic sequence that delivers value fast while keeping governance intact.

Risk controls leadership cared about

Faster decisions only matter if control improves. These guardrails made scaling safe.

Every recommendation is backed by extracted evidence and decision logic.

Edge cases route to expert review with clear reasons and escalation paths.

Structured notes, overrides, and policy checks logged for governance.

Where expert time moved

The biggest benefit was not replacing underwriters—it was amplifying them.

Higher throughput, stronger consistency, and better governance—with experts focused where they add the most value.

Want to replicate this in your lending operation?

Share your current underwriting flow. We’ll respond with a high-level blueprint: what to automate, where humans must remain in control, and the fastest path to measurable impact.